Why have these three stocks historically commanded approximately the same True Worth™ price earnings ratio?

- SCANA Corp. (SCG), a public utility, has a historical earnings growth rate averaging 3.2% per annum, VF Corp.

- (VFC), an apparel manufacturer, has a historical earnings growth rate averaging 7.4%, and United Technologies Corp.

- (UTX), an aerospace and technology conglomerate, has a historical earnings growth rate averaging 13.3%.

Even with such wide discrepancies in growth, each indicate an implied fair value PE ratio of 15.

The following price and earnings correlated F.A.S.T. Graphs™ and accompanying performance charts illustrate this point. However, note that even though their intrinsic values are represented to be similar, the rates of return their shareholders have received had differed greatly.

So the question is, with such different rates of earnings growth, how do you justify all of them having the same fair value calculation? The remainder of this article will deal with answering this important question.

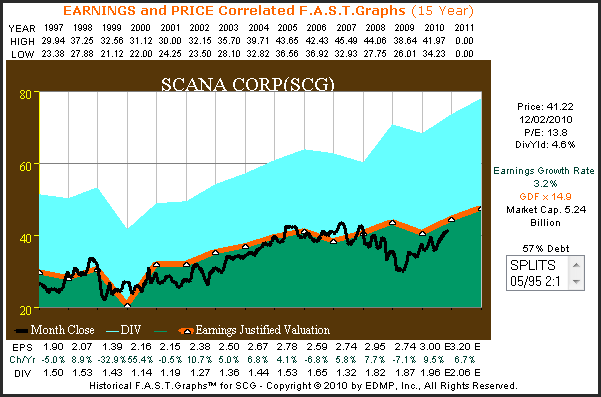

(SCG): 15 year earnings and price correlated F.A.S.T. Graph™

The orange earnings justified valuation line on Scana Corp. (SCG) calculates out at a PE ratio 14.9 (15 rounded) utilizing Ben Graham’s famous formula for valuing a business. The PE ratio is marked in orange to the right of the graph with the letters GDF (Graham Dodd formula) in orange which is color-coded to the line.

Note how the stock price has tracked the earnings line over time. Anytime the black price line is below earnings, it tends to move up towards the earnings line and vice versa. The blue shaded area represents dividends paid out of earnings. Therefore, an investor behaving rationally might not want to pay anything over 15 times earnings, and probably less, before they bought this company. The main point is that the orange line represents a good barometer for value.

click to enlarge images

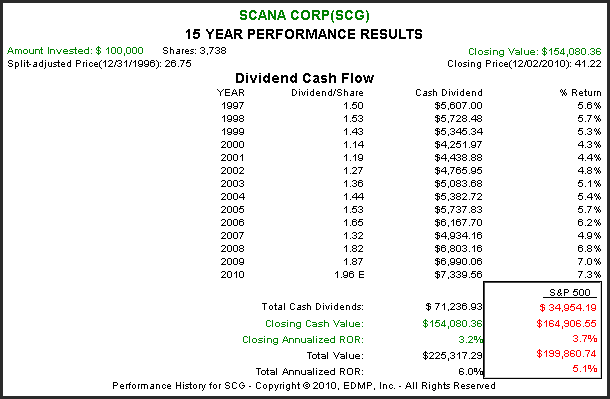

On the performance graph below, notice how the Closing Annualized ROR (capital appreciation) is identical to the earnings growth rate above. Furthermore, notice how beginning and ending valuations were similar and, therefore, earnings growth and total return are virtually the same. Also, notice how dividends contribute significantly to Total Annualized ROR (total return).

(SCG): 15 year performance results SCG

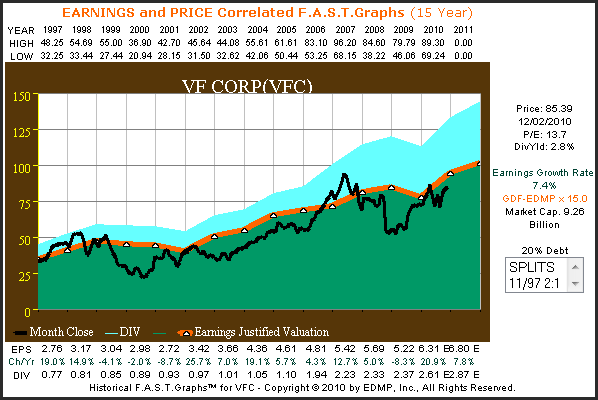

(VFC): 15 year earnings and price correlated F.A.S.T. Graph™

VF Corporation (VFC) also shows their stock price closely tracking the orange earnings justified valuation line, which at 15 times earnings, is the same as SCANA above, even though their earnings growth rate is more than twice as fast at 7.4%. The earnings justified valuation line on this company is calculated utilizing a modified version of Ben Graham’s famous formula and the PEG ratio formula that applies to fast-growing companies (15% earnings growth or better).

This graph is marked by orange letters, color-coded to the earnings line of GDF-EDMP indicating the use of this different formula. Once again we see that whenever price gets above the valuation line it soon moves back to it, and vice-versa. Just like with SCANA Corp., a rational investor considering VF Corporation would not want to pay more than 15 times earnings to buy it. If they could pay less, a case can be made that it would be a bargain.

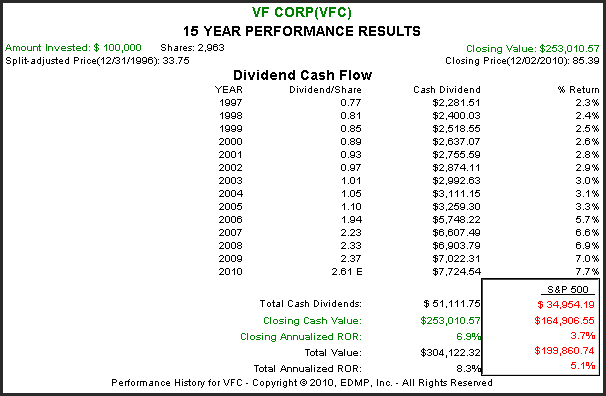

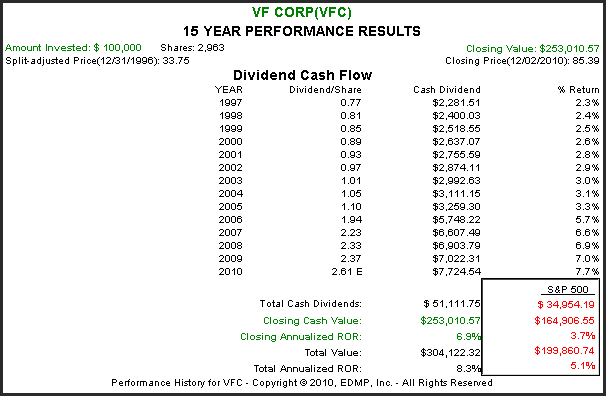

Shareholder Closing Annualized ROR (total return) on VF Corporation since 1997 of 6.9% correlates very closely to the earnings growth rate of 7.4% noted above, with only a modest adjustment based on slight undervaluation currently. Dividend income on this faster growing, but lower yielding company, grow faster and make a meaningful contribution to total return. However, notice that total dividend income is less than the total dividend paid by SCANA Corp., but total return but is greater due to faster earnings growth.

(VFC):15 year performance results VFC

{kind=link}

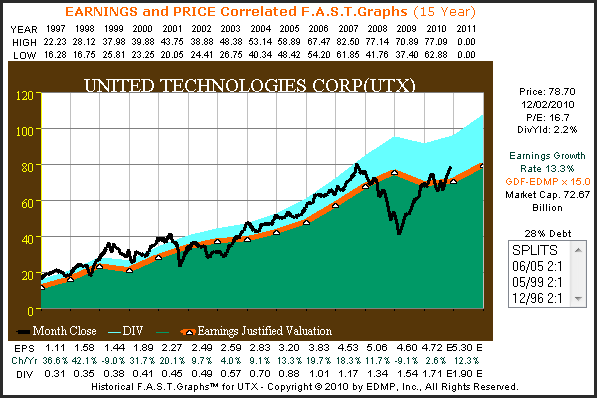

(UTX): 15 year earnings and price correlated F.A.S.T. Graph™

United Technologies Corp. (UTX) provides a third example where the fair value price earnings ratio still calculates out to be 15 times earnings, even though earnings growth at 13.3% is close to double what VF Corporation grew earnings at. However, we still use the modified GDF-EDMP valuation formula as growth remains between our 5% to 15% threshold. Once again, note how this calculation of fair value provides an intelligent barometer at which to consider investing in this company at. It may not be perfect, but it certainly serves as a good guide.

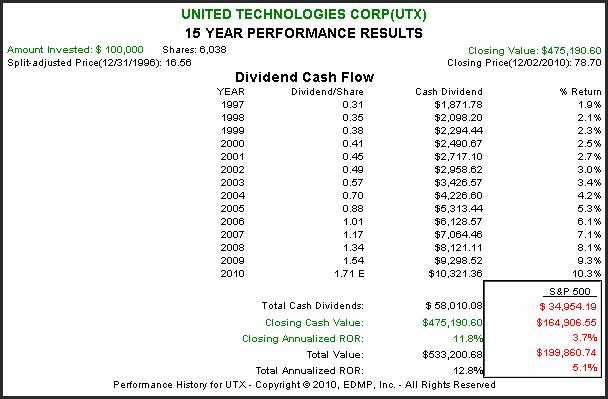

Faster earnings growth generated by United Technologies Corp. since 1997 generates a higher total return for shareholders than the previous two examples. Most importantly, the correlation between earnings growth and return is evident. Overvaluation at the beginning of this measured time frame, which is greater than the current overvaluation, accounts for the slightly lower than growth rate return. Nevertheless, the correlation is clear.

(UTX): 15 year performance results UTX

{kind=link}

“Price Is What You Pay. Value Is What You Get.”

The venerable investor Warren Buffett has a real knack of putting complex concepts and ideas into simple and easily understood terms. In our opinion, his quote, “Price is what you pay. Value is what you get” is one of the more profound and important statements he has ever uttered. If truly understood, these simple words represent perhaps some of the most important bits of investment wisdom that an investor could ever receive.

The concept of value represents the key to receiving the full benefit that these wise words provide. Knowing the price you pay is simple and straightforward. And, although many have an intuitive understanding of value, its deeper meaning is often only vaguely comprehended. Anyone who has truly made the effort to study Warren Buffett’s investment philosophy understands that receiving value on the money he invests is of high importance to him.

So how do you know, when buying a stock, if you’re getting value or not for your money? We contend that the answer lies in the amount of cash flow (earnings) that the business you purchase is capable of generating on your behalf. And regardless of how much cash flow the business can generate for you, its value to you will be greatly impacted by the price you pay to obtain it. If you pay too much you get very little value, but if you pay too little then the value you receive is greatly increased.

Therefore, if value is what you’re looking for, then it’s important that your attention be placed on the potential cash flows that you’re expecting to receive. Unfortunately, few investors possess the presence of mind to focus on this critical element. Instead, investor attention is more commonly and intensely placed on stock price and its movement. A rising stock price is usually considered to be good, and a falling stock price considered bad.

Another investing great offered his view on this important point: “Just because you buy a stock and it goes up does not mean you are right. Just because you buy a stock and it goes down does not mean you are wrong.” Peter Lynch ‘One Up On Wall Street’

Just like the Warren Buffett quote that this article is based on, Peter Lynch’s quote is also based on the principle of sound valuation. The point is that a rising stock may be dangerously overvalued, while the falling stock price may indicate that the company is becoming a rare opportunity on sale.

Knowing the difference will materially impact not only the rate of return the investor receives, but perhaps more importantly, the risk they take to get it. As we will illustrate later in Part 3 of this series, you can dramatically overpay, for even the best company. It is a truism, that the stock market can and will grossly mis-price a security from time to time – up or down.

From what has been said so far, it should be clear that in order to receive value; you have to know how to calculate value. Then, and only then, can you be absolutely certain that you’re investing in a stock and receiving value for the price you pay. However, there is an important caveat that needs to be introduced.

As the three example companies above illustrate, just because you buy a stock at value doesn’t necessarily mean that you will receive a high return. This is because value, although an important one, is only one component of future return. As we illustrated by the above examples in this article, the other important component is earnings growth rate.

To clarify, you can buy a slow-growing company at sound valuation and even at the same valuation as a faster growing company, while still earning only a modest rate of return. In fact, it could be argued that only being willing to invest at sound valuation is more critical for a slow grower than it is for a faster grower.

The rationale here is that there is very little margin for error when investing in a low growth security. Therefore, it’s even more imperative that you get valuation correct. This may be one of the most confusing aspects of valuation, or value, that we will attempt to elaborate.

The Foundational Principles of Value

The principles that valuation is based on can be represented mathematically. However, in our first article in this series, on how to value a common stock, we promised that we would not bore the reader with complex mathematical formulas. Instead, our objective is to provide logical explanations of value that represent its essence.

Therefore, we believe the reader can possess a more practical and useful understanding of the principle called “value”. In order to receive value when you buy a stock, you have to be careful that you are only paying a price that represents sound valuation.

Furthermore, the terms value and valuation, though not synonymous, are very closely related. We are going to do our best to illustrate that the investor can only get value when buying a stock if they apply the discipline of sound valuation when they do.

In other words, when the price you pay is at a level that equals sound valuation, then good value is what you will receive. As previously suggested, if you overpay your value will be less, and if you’re fortunate enough to buy on the cheap, your value will be enhanced.

How Do You Value Zero Growth?

Let’s start by looking at sound valuation from the perspective of minimum to maximum levels based on rates of growth. The reader should understand that much of what we will present next represents a very overly-simplistic view of valuation. However, we believe that this is the best way to lay a sound foundation of understanding of this important investing principle.

There will be subtle calibrations that investors need to apply when actually making investments in real world situations. On the other hand, the core principle will aptly apply and hold true. Let’s initially look at how you would value a future stream of income that doesn’t grow. A 10-year treasury bond would represent a good proxy to illustrate this principle. The interest rate is fixed and guaranteed, but it does not grow.

Common sense and logic would dictate that you would never be able buy a treasury bond at one times its interest. In other words, a stream of income has value that is a multiple of its annual income stream. In order to calculate current valuation, you simply divide the interest rate it pays into its price. With 10-year treasuries yielding approximately 3% today, you divide 3 (the rate) into 100 (the price) and discover that it is selling at approximately 33 times interest.

Historically, this is a very high price which means that yields are also historically low. Therefore, people, recently traumatized by the great recession that are buying treasury bonds today are willing to pay the high price, for the safety they perceive they are receiving. Under more normal levels of interest rates, 10-year treasury bonds have more typically been offered at yields of 6% to 8%. Do the division and this calculates to valuations of approximately 12 to 17 times interest.

Common stocks are certainly not as safe as treasury bonds; however, the principles behind sound valuation still apply. In other words, as long as a company generates an income stream, even if it doesn’t grow it will have value that is greater than its annual rate. Otherwise, this no growth investment would be generating cash on cash returns of 100%. Clearly, this would be illogical. Consequently, just like a treasury bond trades at a multiple of interest, a common stock will trade at a multiple of its income stream which is generally represented as earnings.

The reason we started with looking at a safe but no growth fixed income vehicle was to establish the minimum foundation of valuation. Historically, the average price earnings ratio that has been applied to the average company (the S&P 500) for the past 80 years has been 15. In order to keep our promise of keeping it simple, we merely point out that this valuation relates to normal fixed income yields of 6% to 8% as discussed above.

Most importantly, this 15 multiple should be thought of as a barometer used as the starting point for valuation calculations and not an absolute number. However, this helps explain why our three examples, each with different earnings growth rates, have approximately the same fair value PE of 15.

How Do You Account for PE Ratios Below 15?

Anytime you come across a company whose price earnings ratio is less than 15, which we’ve attempted to establish as a foundational PE ratio in this article, it’s usually associated with uncertainty. A current PE ratio below 15 normally implies a concern that future earnings are going to be less than current levels.

In other words, this would imply that you are paying a higher PE ratio for these expected lower future earnings. Also, a PE ratio below 15 may just be an example of the market mispricing the company as we pointed out earlier in this article.

For example, let’s assume you buy a dollar’s worth of earnings today and pay $15, or a PE ratio of 15 to buy them. One year later, the dollar’s worth of earnings you paid $15 for today have fallen to only $.50 worth of earnings. Therefore, you have paid a price earnings ratio of 30, or twice as much to buy these future earnings. Consequently, the market may be acting as a discounting mechanism or as suggested just mispricing the company.

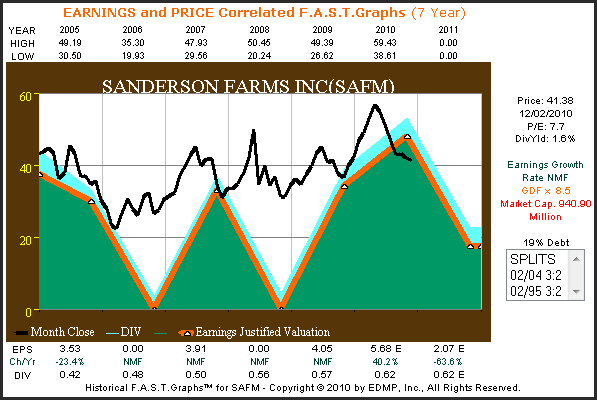

(SAFM): 7 year earnings and price correlated F.A.S.T. Graph™

The example of Sanderson Farms Inc. (SAFM) below may represent an example of uncertainty. Clearly, earnings since calendar year 2005 have been very inconsistent and are expected to fall from $5.68 for fiscal year 2010 to only $2.07 for fiscal year 2011. The current price of $41.38 indicates a current PE ratio of only 7.7 against today’s five dollars’ worth of earnings; however, current price would represent a PE ratio of approximately 20 times fiscal 2011 earnings of $2.07. No research has been conducted on this company. Therefore, these comments are made solely on the backdrop of what the graph below shows.

Conclusions

In this Part 1 of this three-part article on value is what you get, we attempted to lay the foundation of understanding how to value a common stock. So far we have looked at low to moderate earnings growth examples and commented on collapsing earnings which really have no value. In Part 2 we will look at companies that grow earnings at 15% or greater as we investigate the nuances of valuating this faster growth.

In both Part 1 and Part 2, we are focusing on historical evidence only, in order to establish the validity of our thesis. In other words, theories are fine but need to hold up in the real world. This is the real value that historical analysis offers, actual real world evidence that the theories hold up. In Part 3 we will change our focus and look to valuing the future. Applying the same logic that we learned from the past, should enable us to make better decisions about the future.

Disclosure: Long SCG, VFC, UTX at the time of writing.

The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.