Introduction

Finding attractive investments in the dividend growth space has become a real challenge in today’s overheated market. This is especially true if you limit yourself to looking in the obvious places. Simply stated, you won’t find any bargains today in the Procter & Gambles, Johnson & Johnsons and Coca-Colas. In other words, the flight to quality and quest for yield has driven the classic Dividend Aristocrats and Champions to lofty valuation levels. Perhaps even more importantly, you won’t find a lot of growth potential with the blue-chip stalwart dividend growth stocks either. Here I am referring to both capital appreciation potential and dividend growth.

Nevertheless, my primary investment focus today is searching for attractive valuation, above-average current yield, dividend growth and some long-term capital appreciation potential. Since I am not finding any of those attributes by looking in the obvious places, I had to broaden my search. My willingness to look beyond the obvious places also stems from my belief that it is a market of stocks and not a stock market. This belief suggests that regardless of whether we are in a bull market or a bear market, there will always be attractive stock investments to be found. Today’s bull market is proving to be no exception.

Penske Automotive Group looks like a very attractive investment opportunity with an above-market current yield, low valuation and above-average growth potential. Since I currently consider these to be the most important attributes to attract my interest, I feel this mid-cap dividend growth stock is worthy of a closer look. Therefore, with this article, I will share what I have learned about this company so far. My research and due diligence process is not yet complete, but I am very intrigued by what I have discovered thus far.

Penske Automotive Group (PAG)

Simply stated, Penske Automotive Group operates numerous premium auto dealerships throughout the world. In 2016, North America provided 60% of their revenues and the U.K. 32% with the remaining 8% from other international markets such as Australia and New Zealand. Over 93% of their worldwide revenue comes from retail automotive, 5% from retail commercial truck and the remaining 2% from commercial distribution and other.

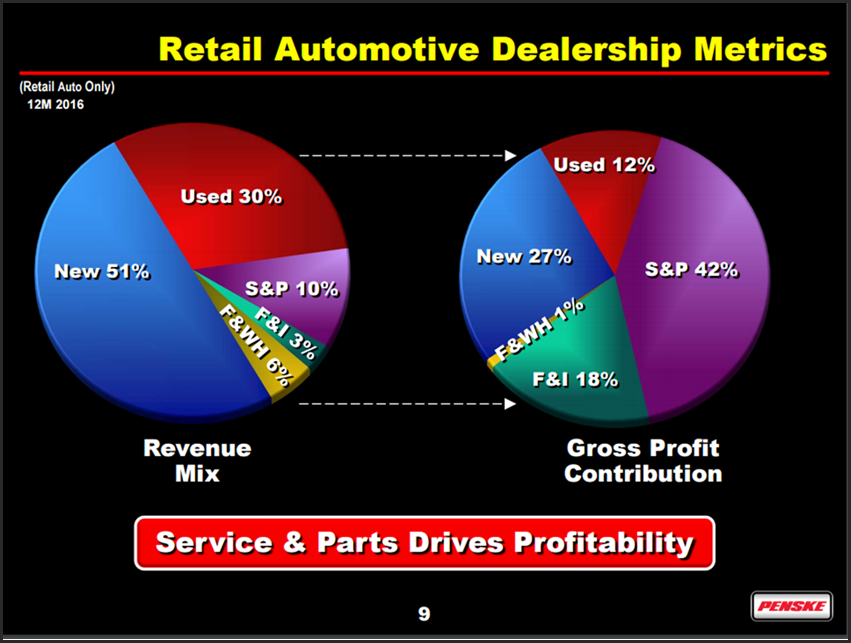

However, I found their revenue mix and profitability both balanced and interesting. As the slide below depicts, 51% of their revenue is derived from new auto sales, 30% from used auto sales and 10% from service and parts. But what I found more interesting was that 42% of their profitability came from service and parts. This struck me as a stable base for profitability because warranty work on new cars go through the dealership, and owners of premium vehicles tend to keep using the dealer for service after the warranty expires.

Another area that I feel bring stability and growth potential is the fact that 72% of its retail automotive dealership revenue comes from premium brands. This suggests that they deal with a more affluent customer that is less likely to be as affected by recessions or weaker economies. The following slide breaks down their revenues by brand.

Regarding future growth, Penske is expected to generate most of its growth from acquisitions. This growth-by-acquisition strategy seems to make sense due to the consolidation and fragmented nature of the dealership business. The following quote from Morningstar provides additional detail:

“Most growth will come from acquisition because Penske is a rollup dealer. Penske has moved into heavy-truck distribution in Australia and New Zealand, but that is only 2% of revenue, and just started used vehicle stores. The National Automobile Dealers Association reports that as of mid-2016, the number of new-car dealerships was 16,680, down from 25,025 in 1987. This highly fragmented industry has been consolidating because smaller players cannot compete with the scale and cost savings achieved through rollup acquisitions pursued by the six public franchise dealerships.”

Penske management is committed to growing through acquisitions as evidenced by the following excerpt from their 2016 annual report:

“Grow Through Strategic Acquisitions

We believe that attractive retail automotive acquisition opportunities exist for well-capitalized dealership groups with experience in identifying, acquiring and integrating dealerships. The fragmented automotive retail market provides us with significant growth opportunities in our markets. We generally seek to acquire dealerships with high-growth automotive brands in highly concentrated or growing demographic areas that will benefit from our management expertise, manufacturer relations and scale of operations, as well as smaller, single location dealerships that can be effectively integrated into our existing operations. Over time, we have also been awarded new franchises from various manufacturers. In 2016, we acquired or were granted open points representing twenty-seven franchises, which generated approximately $700.0 million in annualized revenue.

We believe there are attractive retail commercial truck acquisition opportunities. We see continued growth in the brands we represent at our existing retail commercial truck dealerships and believe there are opportunities for us to continue to make strategic acquisitions over time. In 2016, we acquired seven retail commercial truck dealerships, six of which we retained, which generated approximately $170.0 million in annualized revenue.”

The following excerpt from their 4th quarter press release summarizes their acquisition results for 2016:

“Acquisitions and Open Points

During the twelve months ended December 31, 2016, the company had acquisitions or opened new dealerships representing approximately $700 million in estimated annual revenue. Subsequent to December 31, 2016, the company completed the acquisition of U.S.-based CarSense , a specialty retailer of used vehicles, which is expected to generate $350 million in estimated annual revenue and accretion of $0.07 to $0.09 in earnings per share on an annualized basis.

Additionally, in January 2017, the company announced that it has signed an agreement to acquire CarShop , one of the U.K.’s leading retailers of used vehicles. CarShop has five large-scale retail locations operating in Cardiff, Swindon, Northampton, Norwich and Doncaster, plus a 15-acre vehicle preparation center. The acquisition is subject to certain conditions and is expected to close by the end of the first quarter of 2017. CarShop is expected to generate estimated annualized revenue of approximately $340 million with accretion estimated to be $0.07 to $0.09 per share on an annualized basis.”

Penske Automotive Group: Compelling Fundamentals and Valuation

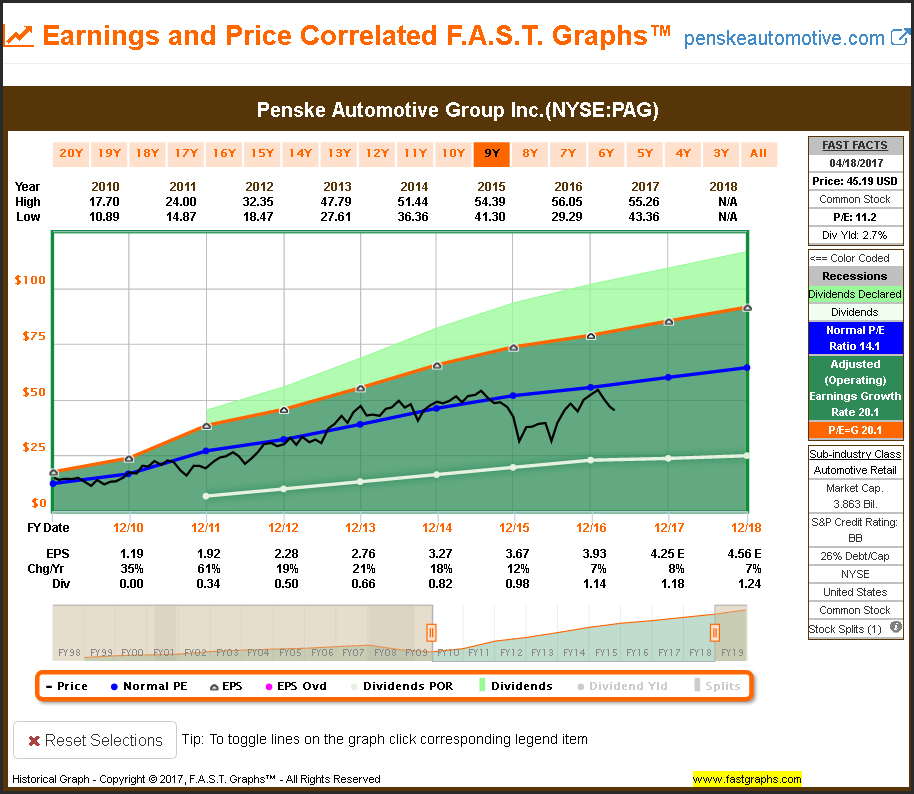

The following earnings and price correlated F.A.S.T. Graphs™ since 2010 illustrates why I became attractive to this dividend growth stock. The orange line on the graph represents a P/E ratio of 20.1 which is also equal to its earnings growth rate average since 2010. The dark blue line represents a historical normal P/E ratio of 14.1.

The reader should note that the market has historically tended to value this company within a P/E ratio range of approximately 13 to 14. Consequently, I consider a P/E ratio of 14 or below for this company as a sound and attractive valuation. Therefore, the current blended P/E ratio of 11.2 indicates that Penske is currently undervalued.

Penske Automotive Group Performance

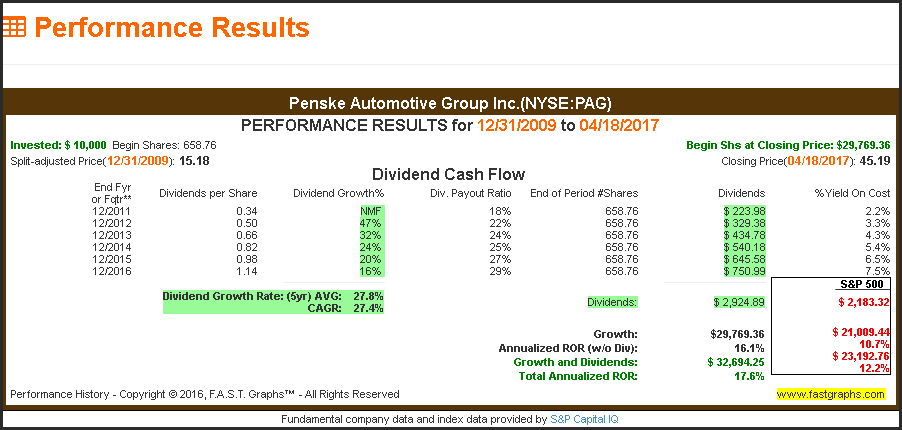

The associated performance results for Penske since December 31, 2009 show significant market outperformance in spite of the current undervaluation. I attribute this to sound valuation at the beginning of this timeframe coupled with earnings growth of 20%. Furthermore, since initiating a dividend in 2011, the company has increased its dividend every quarter for 23 consecutive quarters. Additionally, the company’s payout ratio is low and management has indicated a commitment to paying out approximately 30% of earnings.

Penske Automotive Group: F.A.S.T. Graphs Fundamental Analysis

The following video takes a deeper look at the fundamentals underpinning Penske Automotive Group. In the video, I will take a deeper look into earnings, dividends, free cash flow, and other important fundamental metrics. Furthermore, I also provide my specific expectations of the rate of return opportunity and dividend growth potential that I believe Penske Automotive Group offers at current levels:

Summary and Conclusions

As the title of this article indicates, I believe that Penske Automotive Group is a very attractive mid-cap dividend growth stock hiding in plain sight. Perhaps it’s because the company is small, but I found it odd the company is so lightly followed – especially considering its excellent fundamental attributes. Nevertheless, the more I look at it, the better I like Penske Automotive Group. For me, it offers most everything I am currently looking for: Low valuation, above-average current yield and well-defined prospects for continued growth.

On the other hand, since I started conducting my initial research on Monday, April 17 the stock price has risen dramatically. Fortunately, it is still undervalued in spite of its recent run up. Nevertheless, I feel I need to accelerate my due diligence process before it’s too late. Perhaps many of you might want to join me. Personally, it appears to me to be a very worthy dividend growth stock research candidate.

Disclosure: No position

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.