As our population ages, the quest for income to fund retirement has never been greater.With interest rates at or near all-time lows, the traditional fixed income option does not provide enough yield to meet the needs of most people desirous of living off their portfolio income.Consequently, investors are compelled to search out alternative options.

Royalty Trusts are an option that on the surface offers enticing yields. However, closer scrutiny may tell a very different story. Therefore, the purpose of this article, to rephrase a famous Waylon Jennings song lyric, is to enlighten investors so that they are not looking for yield in all the wrong places.

In our previous article in this series we covered Master Limited Partnerships (MLPs) that primarily invest in the energy sector.Investing in energy assets is one thing that Royalty Trusts have in common with Master Limited Partnerships (MLPs).But Royalty Trusts are really not operating businesses; instead they are financing vehicles.Therefore, Royalty Trusts are typically run by banks.

Although they trade like stocks, they have no management and no employees.Specific energy assets, which typically might be oil, coal and or natural gas are placed into the trust.

Even though the Royalty Trusts we will cover in this article trade on the New York Stock Exchange, technically they are not stocks; instead, they are investment trusts. They buy the right to receive royalties on the production and sale of natural resource assets and then pass on the profits to the trust unit holders (shareholders).

Just like any other trust, a Royalty Trust is a legal instrument that is created to hold assets for others.Therefore, a typical Royalty Trust is a legal entity that holds ownership of an asset (asset-backed security) and passes through the income to its investors known as unit holders.

Consequently, in contrast to a Master Limited Partnership (MLP), the Royalty Trust can be thought of as a direct play on the underlying commodity the trust holds. Therefore, the distributions (dividends) can vary wildly as they are directly tied to the market prices of the underlying assets.

A simple way for investors to think about their Royalty Trust holdings is that they are just like owning their own oil wells (assuming, of course, that the trust owns oil wells). However, it’s also important that the investor realizes that they own a finite amount of the resource. Every time a barrel of oil is produced, there is one less barrel securitizing the trust assets. Of course, in the energy sector this is known as depletion. So long-term investors in Royalty Trusts need to understand that once all the oil is produced, the asset is gone, and so is the value of their holding and the dividends.

Even though the typical Royalty Trust owns a finite amount of the underlying natural resource, they are often designed to produce income for periods of up to 10, 20 or even 30 years.Also, since the trust is designed to essentially pay out all of its income to shareholders, the distributions can be very substantial.Over time, the unit holder might receive multiples of cash distributions over and above their original investment.To a great extent, this will depend on the price performance of the underlying assets.

During times of rising prices, trust unit holders can expect high and rising yields. Of course, the opposite is also true. Consequently, many Royalty Trusts have seen their distribution yields fall with energy prices over the last few years.

Yields Tied to Commodity Prices

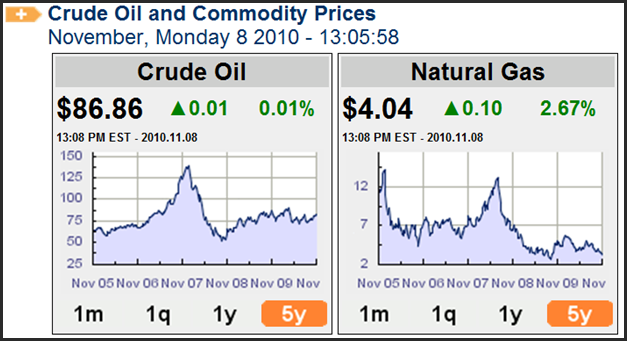

The following graphs reflect the price of oil and natural gas since November of 2005. With oil peaking in early 2007 and natural gas prices peaking in the fall of 2007 there was a direct effect on the yields of Royalty Trusts that invested in oil and gas.

click to enlarge images

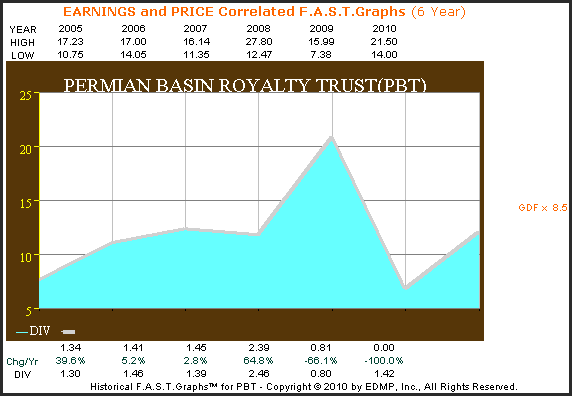

The following F.A.S.T. Graph™ on the Permian Basin Royalty Trust (PBT) plots the cash distributions (dividends) for this Royalty Trust since calendar year 2005. Note how closely the dividends (blue shaded area) correlated to the price of oil in the above crude oil price graph.

PBT 6yr. Earnings and Price Correlated F.A.S.T. Graph™

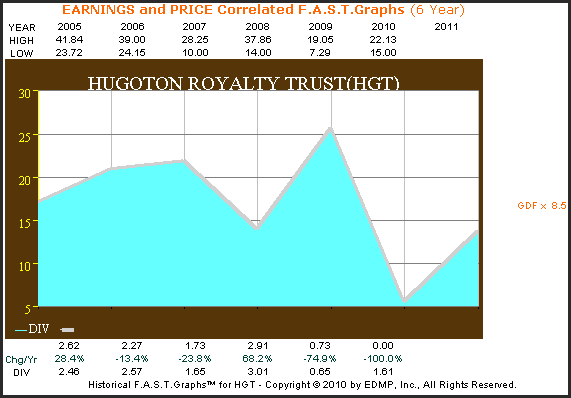

The following F.A.S.T. Graph™ on the Hugoton Royalty Trust (HGT), which predominately invests in gas producing properties, offers a similar correlation of its dividend (blue shaded area) to the price of natural gas as seen in the above natural gas price graph.

HGT 6yr. Earnings and Price Correlated F.A.S.T. Graph™

The primary points of the above graphic presentations were to illustrate the direct relationship between the cash distributions that a Royalty Trust will pay to trust holders and the price of the underlying asset. The distribution rate (dividends) of both trusts rose and fell in close to direct proportion to the rise and fall of the prices of each respective trust’s underlying asset base. At the bottom of each F.A.S.T. Graph™ you can see the dividend rate, and just above it the rate of change from one year to the next (Chg/Yr).

Depleting Assets-The Risks

In addition to the risk of volatile yields, depletion is another potential negative that Royalty Trust unit holders face. Although wide swings in commodity prices and/or production levels can create very inconsistent distribution levels, these same factors can also cause significant changes in the current value of a Royalty Trust. Later in this article we will present examples of Royalty Trusts that richly rewarded their unit holders over intermediate to long periods of time.

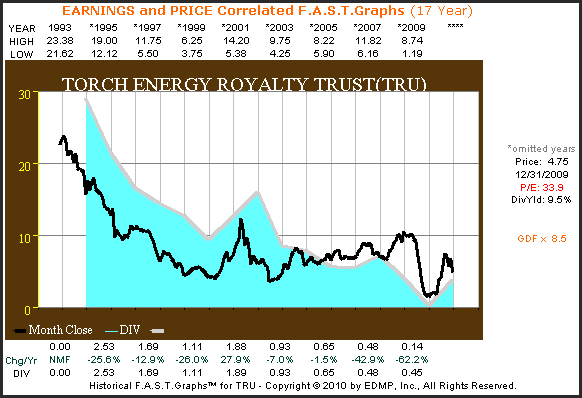

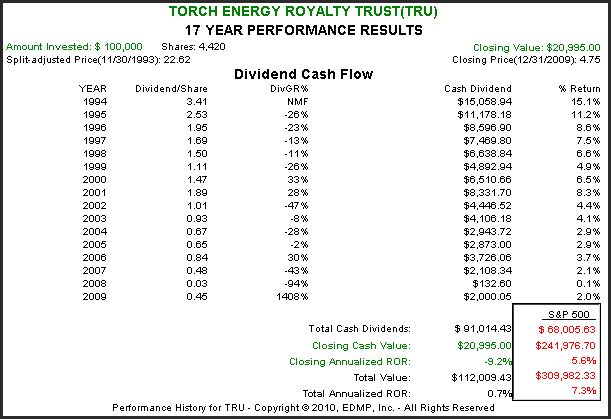

However, first we will review Torch Energy Royalty Trust (TRU) which was formed effective October 1, 1993 and holds net profit interests in oil and gas properties in the Chalkley Field in Louisiana and the Robinson Bend Field in Alabama.This is a trust that has recently announced that it would be terminated and is currently in the windup and liquidation process.

When looked at through the lens of our F.A.S.T. Graphs™ a couple of things become very clear.First of all, the risk of depleting assets can be vividly seen in graphic form. Next, a review of the performance F.A.S.T. Graph™ shows that the trust did not provide returns that unit holders may have expected when they first invested.

TRU 17yr. Earnings and Price Correlated F.A.S.T. Graph™

TRU 17yr. Performance Results

From the F.A.S.T. Graphs™ above it is clear that the Torch Energy Royalty Trust (TRU) saw its share price decline consistently from day one, and so did its dividends (distributions per unit). It would be hard to argue that unit holders of the Torch Energy Royalty Trust (TRU) were adequately compensated for the risk they took.

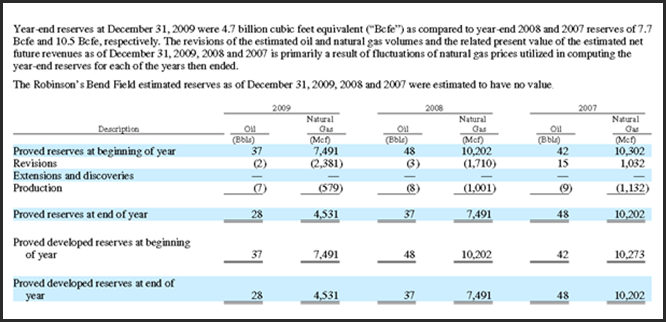

Below are two excerpts from their 2009 annual report that illustrate the risk of depletion. The first speaks to the issue of depletion. Especially note the language that discusses how a portion of each distribution should be considered a return of capital.

The market price for the Trust’s Units may not reflect the value of the Net Profits Interests held by the Trust. The public trading price for the Trust Units tends to be tied to the recent and expected levels of cash distributions on the Trust Units. The amounts available for distribution by the Trust vary in response to numerous factors outside the control of the Trust, including prevailing prices for oil and natural gas produced from the Underlying Properties. The market price of the Trust Units is not necessarily indicative of the value that the Trust would realize if the Net Profits Interests were sold to a third party buyer. In addition, such market price is not necessarily reflective of the fact that, since the assets of the Trust are depleting assets, a portion of each cash distribution paid on the Trust Units should be considered by investors as a return of capital, with the remainder being considered as a return on investment. There is no guarantee that distributions made to a Unitholder over the life of these depleting assets will equal or exceed the purchase price paid by the Unitholder.

This second excerpt in chart form from their 2009 annual report shows how both the estimated reserves of oil and natural gas have been steadily declining (this excerpt only covers the period 2007 to 2009).

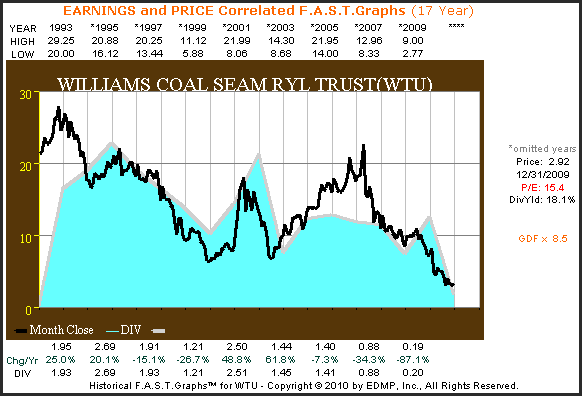

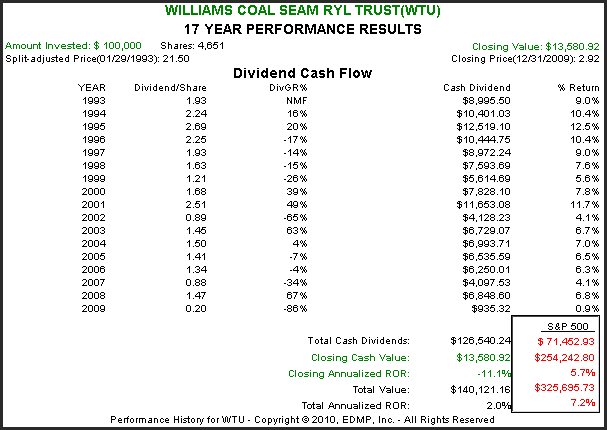

Williams Coal Seam Royalty Trust (WTU)

Williams Coal Seam Gas Trust (the “Trust”), incorporated in 1992, was formed to acquire and hold certain net profits interests (Royalty Interests) in proved natural gas properties located in the San Juan Basin of New Mexico and Colorado. The only assets of the Trust, other than cash and temporary investments being held for the payment of expenses and liabilities and for distribution to Unitholders, are the Royalty Interests.

Williams Coal Seam Royalty Trust is another example of a trust terminating due to depletion. On February 5, 2010, they announced:

That pursuant to the terms of the trust agreement, trust will be required to terminate effective March 1, 2010 because the reserve report as of December 31, 2009, reflects that, as of such date, the net present value (discounted at 10 percent) of the estimated future net revenues (calculated in accordance with criteria established by the Securities and Exchange Commission) for proved reserves attributable to the royalty interests but using the average monthly Blanco Hub Spot Price for the past calendar year less certain gathering costs (the “Termination Present Value” as defined in the Trust Agreement) is equal to or less than $30 million thereby triggering a termination of the Trust.

On November 5, 2010 they announced a liquidation distribution of approximately $2.38 payable November 29, 2010. This information is not included in the F.A.S.T. Graph™ below. However, as you can see by the performance up through 2009, this Royalty Trust is another example that did not adequately reward shareholders for the risk they took.

WTU 17yr. Earnings and Price Correlated F.A.S.T. Graph™

WTU 17yr. Performance Results

Three Prominent Royalty Trusts

The next section of this article will look at three prominent Royalty Trusts through the lens of our F.A.S.T. Graph™ research tool. We will review how they have rewarded their investors since they were formed in the early 1990s based on both price and dividends (distributions per unit). We will look at them in order of worst to best performance. We hope that this will provide the reader with a much more learned perspective on the advantages and disadvantages of investing in Royalty Trusts.

However, a few words about our F.A.S.T. Graph™ tool are in order.Our F.A.S.T. Graph™ tool was designed and programmed to provide essential “fundamentals at a glance” and corresponding performance results on operating companies.Like all computer technology, a research tool is incapable of thinking for itself.Therefore, it’s up to the user to apply their intelligence in order to properly interpret the information presented.

Since Royalty Trusts are not operating businesses in the traditional sense, our F.A.S.T. Graph™ tool requires user interpretations when examining hybrids like Royalty Trusts. However, this does not mean that our F.A.S.T. Graph™ tool is without value when analyzing Royalty Trusts.

Since Royalty Trusts are essentially required to pass through the majority of their royalty income to their unit holders, their distributions per unit can be looked at as the equivalent of earnings-per-share.Therefore, we have drawn the F.A.S.T. Graphs™ on these three companies utilizing an appropriate multiple of cash distributions in lieu of earnings-per-share.

To the right of each graph you will see either the orange letters GDF (Graham Dodd Formula) or the orange letters GDF -EDMP (Graham Dodd Formula modified EDMP version) followed by a number that reflects the appropriate multiple applied to distributions. We then overlay monthly closing stock prices to the light blue shaded area or dividends.

Not only will you find that stock prices are closely correlated to the dividend (cash distributions) of a Royalty Trust, you also find them to be a good proxy for fair value.In other words, if the price is above the blue shaded area (dividends/distributions) it would be logical to assume that overvaluation exists.

One final clarifying point, our F.A.S.T. Graphs™ were originally programmed to provide and calculate estimates based on consensus numbers received from either FirstCall or Zacks. Since analysts do not normally provide forecasts on Royalty Trusts, no logical number could be applied to future distributions per share. Therefore, we have stopped each F.A.S.T. Graph™ at year-end 2009 which represents the last calendar year of actual numbers. Since calendar year 2010 is not complete, we have left it out, even though some distributions have already been paid and received.

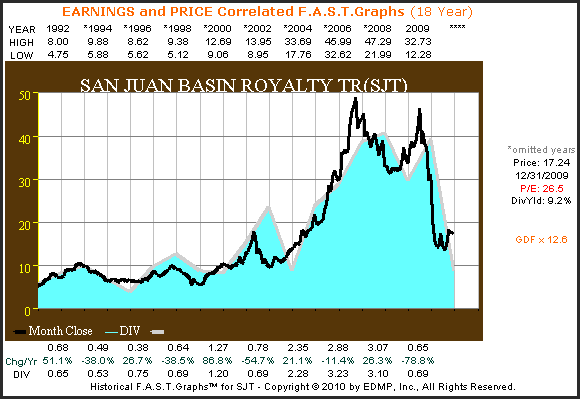

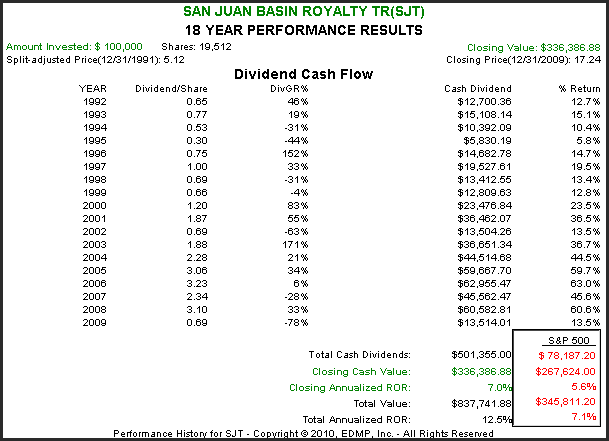

San Juan Basin Royalty Trust (SJT)

The Trust was established in November 1980 by Trust Indenture between Southland Royalty and The Fort Worth National Bank. Pursuant to the Indenture, Southland Royalty conveyed to the Trust a 75% net overriding royalty interest (equivalent to a net profits interest) carved out of Southland Royalty’s oil and gas leasehold and royalty interest in the San Juan Basin of northwestern New Mexico. This net overriding royalty interest (the “Royalty”) is the principal asset of the Trust.

SJT 18yr. Earnings and Price Correlated F.A.S.T. Graph™

SJT 18yr. performance results

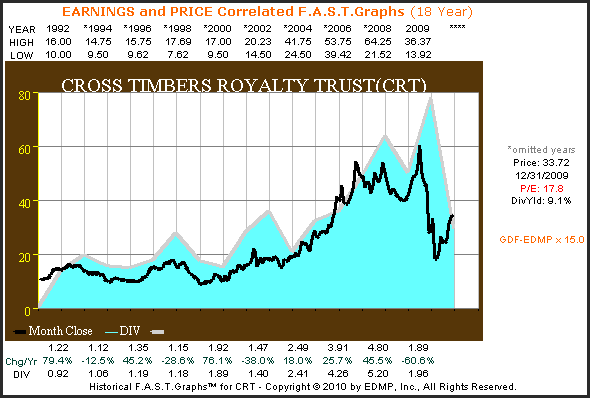

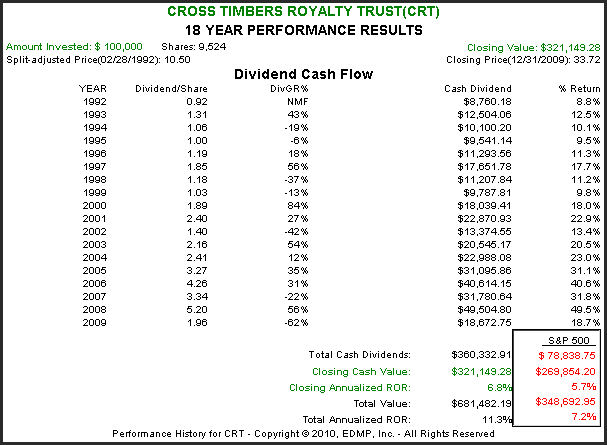

Cross Timbers Royalty Trust (CRT)

Cross Timbers Royalty Trust was created on February 12, 1991 by conveyance of 90% net profits interests in certain royalty and overriding royalty interest properties in Texas, Oklahoma and New Mexico, and 75% net profits interests in certain working interest properties in Texas and Oklahoma. XTO Energy Inc. owns the underlying properties from which these net profits interests were conveyed. The net profits interests are the only assets of the trust, other than cash held for trust expenses and for distribution to unitholders.

CRT 18yr. Earnings and Price Correlated F.A.S.T. Graph™

CRT 18yr. Performance Results

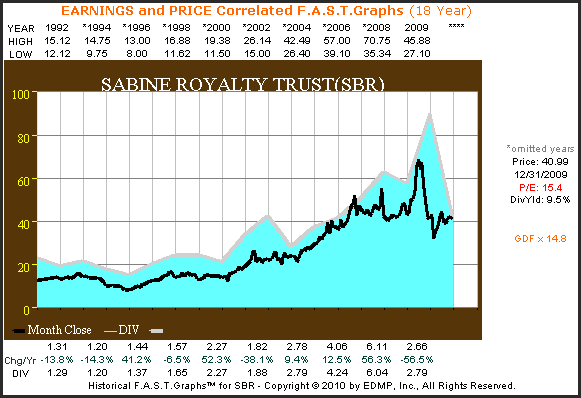

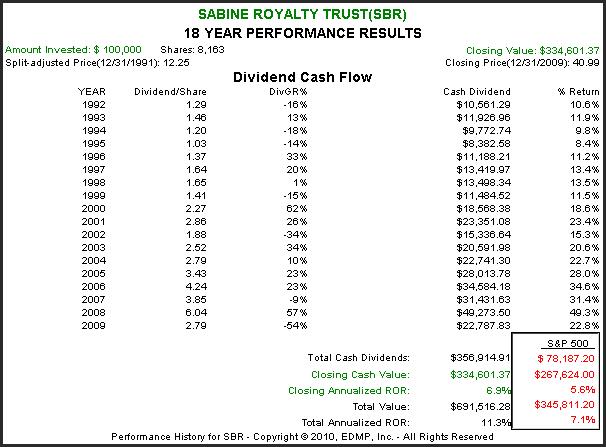

Sabine Royalty Trust (SBR)

Sabine Royalty Trust (the Trust) is an express trust formed to receive Sabine Corporation’s royalty and mineral interests, including landowner’s royalties, overriding royalty interests, minerals (other than executive rights, bonuses and delay rentals), production payments and any other similar,

non-participatory interest, in certain producing and proved undeveloped oil and gas properties located in Florida, Louisiana, Mississippi, New Mexico, Oklahoma and Texas (the Royalty Properties). The conveyances of the Royalty Properties to the Trust were effective with respect to production on

January 1, 1983. The current trustee of the Trust is Bank of America, N.A.

SBR 18yr. Earnings and Price Correlated F.A.S.T. Graph™

SBR 18yr. Performance Results

As you can see from the performance charts on the three examples above, Royalty Trusts can be very rewarding investments for their shareholders. Long-term owners of the above trusts received cash distributions that were multiples of their original investment. Furthermore, if the reserves are adequate, the valuation of the trust shares can provide capital appreciation. On the other hand, the two examples of terminating trusts illustrate the pitfalls that investors can face with this asset class.

Tax Considerations

Similar to the Master Limited Partnerships (MLP), Royalty Trusts provide tax advantages and complexities. Consequently, Royalty Trusts may not be appropriate investments to hold in retirement plans. This is not to say that they can’t be, it merely means that many of the tax advantages offered by Royalty Trusts would be lost if held in retirement plans. If not held in a retirement plan, then additional tax filings and schedules may be required.

Also, certain state filings in the states that the Royalty Trust generates its royalties from may also apply. Therefore, consulting with a tax expert is highly suggested before investing in these unconventional equities.

Conclusions

With the appetite for yield at a heightened level many investors are searching for alternatives to traditional income-producing asset classes. Historically, investors have been attracted to Royalty Trusts because of their exceptionally high yields.

However, since the price of oil and gas has fallen in recent years, the often double-digit yields historically associated with Royalty Trusts have mostly fallen into the single-digit category. Nevertheless, compared to other asset classes, they remain high by today’s standards.

Forecasting future distributions and values for Royalty Trusts is rather straightforward. The researcher has to forecast future prices of the underlying asset class and calculate the estimated recoverable reserves that the trust still holds. Multiply future estimated prices, times the estimate of reserves should provide a reasonable estimate of future value.

Maybe this task is straightforward, but it’s certainly not easy. Therefore “caveat emptor” applies. If you think oil and gas prices will rise from here you might want to take a closer look at Royalty Trusts. Hopefully, this article has provided an intelligent framework from which to execute a rational analysis. Our next article will look at real estate investment trusts or REITs.

Disclosure: No positions at the time of writing.

The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.